No. 1 - Economic Change & Personal Experience in Central Maryland Since 2000

No. 1 - Economic Change & Personal Experience in Central Maryland Since 2000

Part I: Where I'm Coming From & the Great Recession in Maryland

The builders have picked up their shovels in Maryland. Cajoled, at long last, by the recent bounding pace of economic growth in the state between D.C. and Baltimore, these planners, developers, architects and contractors have brought something not seen in quite some time to the Old Line State – a renovation of the built environment, new neighborhoods, lecture halls, office parks, and glitzy, pedestrian shopping centers presenting a bold vision of what a suburban ecosystem ought to be. And now this rolling stone of bricks and draft plans presents me, whose vision of Central Maryland was frozen in the lows of recessionary apathy, with a jarring experience of coming home again.

As in the rest of the country, the years between 2015 and the outbreak of the pandemic were quite the economic boon for Maryland – jobs, wages, homeownership, and employment all ticked up smoothly.

This phenomenon was no less present in the low-scale urban, suburban and exurban areas of Central Maryland, which for the purposes of this piece I'll describe as a rough rectangle finding its southwestern edge at the border with Washington DC, its eastern edge on the Chesapeake Bay, its northeastern border on the exterior of Frederick, MD and its closure around Baltimore in the northwest.

I lived most of my life as a kid within the interior of this imaginary polygon, though this is not an unusual circumstance – construed liberally, 75% of Maryland's population can say the same. And today, many of the friends who grew up here with me have dispersed themselves within this shape to start their adult lives.

I have friends in new build high-rises in the inner ring of booming Frederick; friends in the legacy core of high-profile Bethesda, profiting from a commercial mix tilting more and more towards our tastes; friends roosting in the good, old bones of Baltimore's neighborhoods; and friends in Takoma Park and Silver Spring and Columbia and Annapolis and Ellicott City. My parents gave up the exurbanity of Fairland Road, where my sisters and I were raised, for the newfound vitality of Laurel, where developers have erected a new town in a shockingly small amount of time.

It was not as a matter of course that these new high-rises and renovated shopping districts were ready and waiting for the generation of Maryland millennials aging into their prime years of household formation. Rather, it was only the sustained pressure of a half-decade of post-Recession economic growth that forced builders back onto their job sites in a major way.

I think that surveying the structure and distribution of this growth, and particularly of its impact on the built environment, is a worthwhile exercise. That's what I'll attempt to do in this essay – give a sense for what's changed about incomes and labor, how, and what it's meant.

I'll pay special attention to housing, a topic so dismaying in Marin County and Cheviot Hills and the Upper West Side which obtains an entirely distinct valence in Central Maryland: housing as opportunity, independence, mobility, deliverance.

I want also to convey in this piece the true Unheimlichkeit that this economic growth has foisted upon me, by now an itinerant visitor stopping by semi-annually, on remand from the coastal cities where I'm doing my best to ply a trade and build a career.

That pretentious German word was used most famously by old Freud, best translated for his purposes as "uncanniness", but I'll take advantage of its literal meaning and translate it as "unhominess".

")

It's that unhomey alienation which crops up every time I take a familiar left turn and run for the first time into a pristine, pedestrianized shopping center, full of fast casual eateries and breweries.

It appears when I end up on a night out at one of the casinos never found in the state before 2011, towering like they do in Macau over the rest of the low-slung environment.

It manifests every time I lay my head down to sleep in a cozy family home whose foundation was for many years mere fallow field, the road thereto previously little more than a dead end.

Up the Cliff and Hitting Rock Bottom, 2000-2012

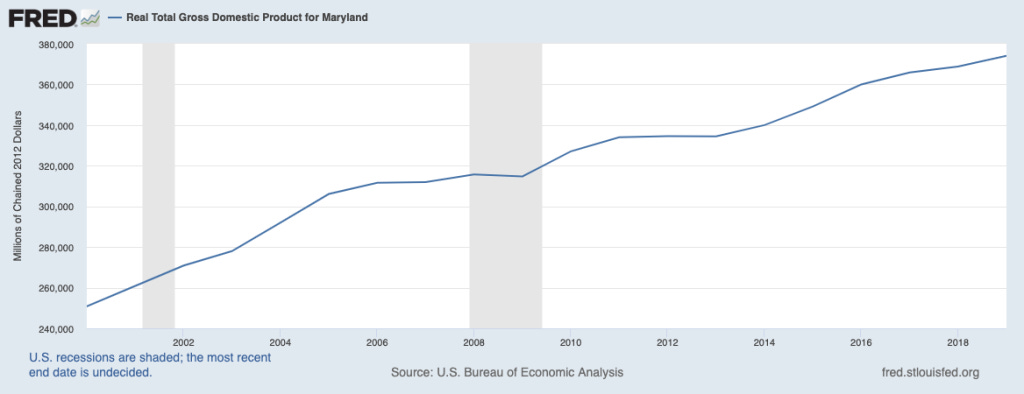

After the turn of the millennium, the economy of Maryland grew like the rest of the nation's, with real state-level income growing from $251bn in 2000 to a peak in 2008 of $316bn.

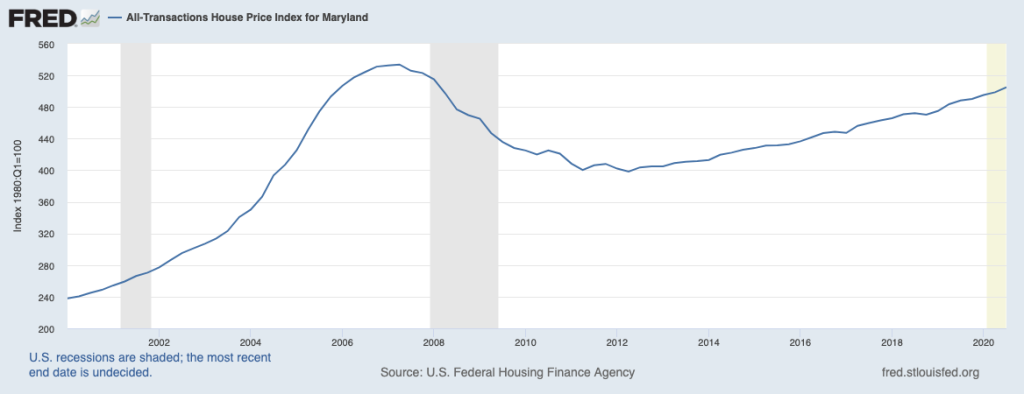

Critical to this Goldilocks 3% annual GDP growth, as elsewhere, was a red-hot housing market. The first half of the below chart illustrates the effect of that red-hot housing market on home prices.

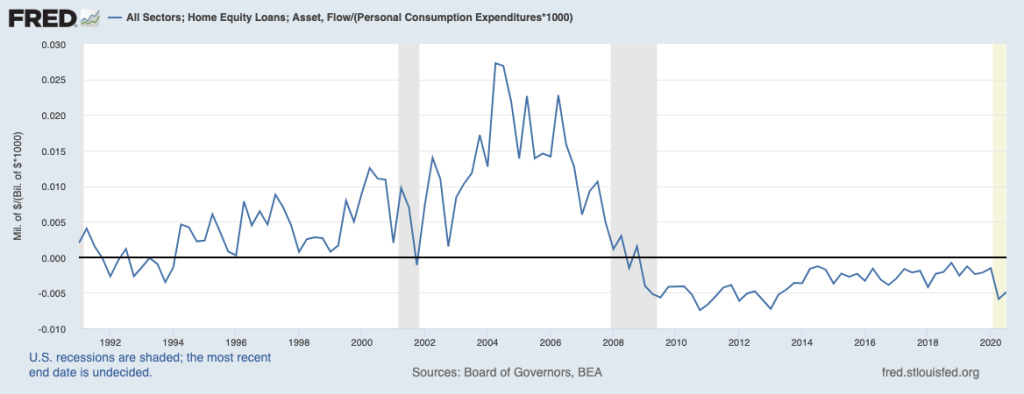

What did everyday homeowners do in response to this major shift in the market for their largest asset? To understand that, we need to look towards one curious feature of the Bush-era economy, namely the outsized influence of an unfettered financial capitalism.

Loosed from its regulatory shackles in the 1980s, the industry's traders and structurers in Manhattan were by the turn of the century releasing truly creative financial products into the world. Case in point: the home equity line of credit.

HELOCs, as their friends call them, allowed existing homeowners to profit from this bubble in home prices by borrowing against the juiced-up value of their own homes. HELOCs distinguished themselves from more prosaic products, like second mortgages, by allowing the borrower to open a revolving line of credit, like a consumer credit card, with a credit limit equal to the value of their home.

The greater acceptance of HELOCs by homeowners and banks nationwide constituted a tremendous expansion of credit to consumers, an expansion which attained the heights in 2005 of financing $3 out of every $100 of household consumption. As HELOC usage grew, so did the dependency of the whole domestic economy on the continued strength of the housing market. That's the tough thing about collateralized debt – the value of the collateral ain't everything, but it's the only thing.

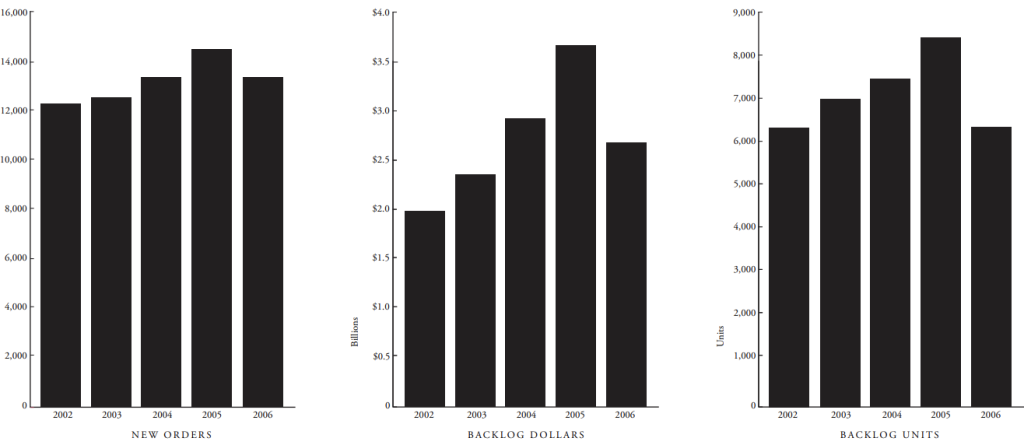

On the other side of the equation, the years-long rise in housing prices naturally impacted the companies whose work consisted in building houses. One of the more remarkable testaments to the strength of the residential real estate market in the early aughts can be found in the annual reports of NVR, Inc.

The folks at NVR are the nation's fifth-largest homebuilder and, under the banner of Ryan Homes, have historically made about one-third of their revenue in Maryland.

In 2005, NVR reported "the most profitable year in the Company's history," making $698mm in profit on $5.3bn in revenue, all the result of "the largest ever volume of new orders and settlements."

Fortune, a one-trick pony magazine if there ever was one, ranked NVR's equity that year as the best investment among Fortune 500 companies over the preceding decade. Times were good for Ryan Homes and its managers.

By the end of 2006, however, the company was cautiously less ebullient, communicating a cyclical shift that economic and financial commentators would take many more years to fully chart out. NVR wrote that it found itself "confronted with the challenges of a marketplace where increased demand and strong price appreciation of the last several years gave way to more difficult market conditions."

As elsewhere, the parabolic swing up in home prices was met with the rowdy pop of the housing bubble. Already unstable by the end of 2006, growth in home prices evaporated and in 2007 and 2008 a distinct decline took over.

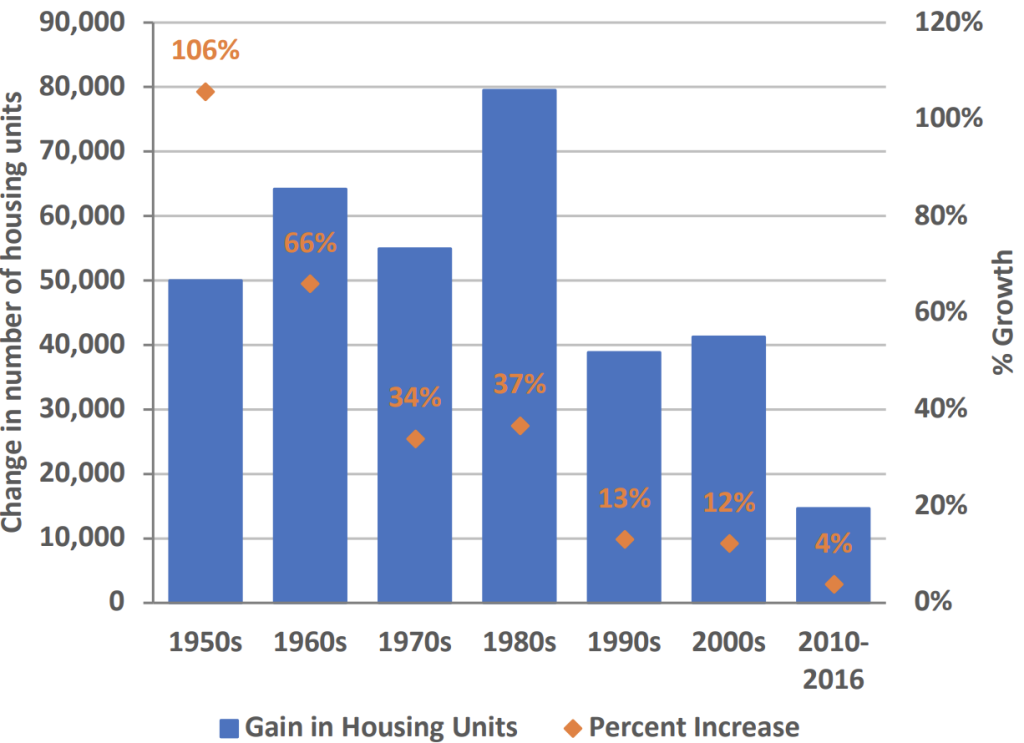

And while homebuilders (and their investors) are used to weathering the cycles of modern capitalism, this time was different: indeed, the years following 2010 were the worst in Maryland for new housing starts since the 1950s.

NVR managed to turn a profit in 2008, the only publicly traded homebuilder to do so, but the effects of the downturn are easily heard in the tone of the introduction to their annual report:

Potential homebuyers were faced with several headwinds, including tighter lending standards, higher unemployment rates, dwindling investment balances, and news of a deepening recession. As a result, consumer confidence fell to historic lows and the demand for new homes weakened significantly. In addition, the housing market continued to experience high inventories of both new and existing homes, as well as high foreclosure rates. All of these factors contributed to the downward pressure on housing prices in all of our markets; and consequently, downward pressure on our profitability.

— from the 2008 Annual Report of NVR, Inc.

Meanwhile for Maryland's homeowners, you can extract from the chart of home prices above their experience as the crisis ebbed on pretty clearly – a distinct feeling of hitting rocks all the way down.

No less acutely felt was the impact of all those outstanding HELOCs in a regime of sinking prices – in September of 2008, Louise Story could already write for the NY Times a gauzy piece about the excesses of the lending market titled "Home Equity Frenzy Was a Bank Ad Come True".

"Little by little, millions of Americans surrendered equity in their homes in recent years as home prices seemed to rise inexorably from one peak to the next," she wrote.

By 2012, the nadir of home prices in the state, CoreLogic reported that Maryland's proportion of mortgages underwater was 9th highest in the nation, within the same realm as the infamous Nevadan housing market.

The housing bubble and its malcontents sucked up most of the air in the real estate developmental room, but this is not to say that there was zero commercial development in the decade approaching the Great Recession. In 2005, a developer razed 8.5 acres of a light manufacturing district immediately off the vital US Route 29 and built Westech Village Corner, there siting 12 "retail commercial businesses," including an IHOP, a TGI Fridays, and, critically for your correspondent, a Panera Bread. When a Chick-fil-A arrived a few years later, it caused a sensation.

In elementary school, we debated, along with the rest of Maryland's chattering class, the merits of infrastructure development under the guise of new highways and new transit lines. And when the corrections came, Maryland's government took the shovels out – I can recall the installation of an overpass at Briggs Chaney Road, and my mighty alma mater, Paint Branch High, was torn down and replaced over the course of my time there. Ours was the last class to graduate from the old building of nooks and crannies, which had opened to serve freshmen for the first time in 1969.

But I hope by the enumeration of these examples to illustrate the meagerness of these changes – one shopping plaza (more parking lot than anything else), a new high school, and some highway construction came together to form the sum of new building in my neighborhood over the course of a long decade.

I imagine this pace to be pretty typical of exurban/semi-rural non-residential construction – the settled patterns of low intensity comings and goings around Central Maryland never necessitated a crush of new building. Prudent administrators could look 5 years out, pick the handful of projects most useful to current or forecast needs, and steadily apply their hand to the completion thereof.

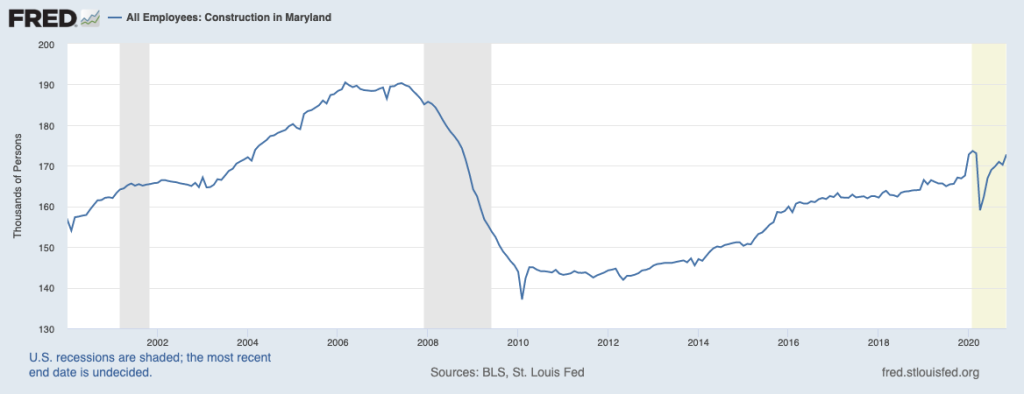

This two-track approach – a volatile, hot residential market partnered with a smoother, slower business and infrastructural construction market – suited the labor market, anyway. Construction employment rose by 50,000 jobs after 2000, accelerating as the housing bubble blew bigger and bigger.

Construction employment didn't stop crashing until home prices did, and even then, the lows stuck around longer than they did in the housing market.

That, then, covers the economic change I promised in the title. What about the personal experience?

I graduated high school and skipped town in 2012, that sullen year of bottoming out, unaware except in a peripheral sense of what was happening to the lives around me. Many of my friends' parents were employed in the federal government – for them, shutdown shenanigans and raise freezes would be the most keenly-felt impact of the recession, at least for the time being.

(To go long on a parenthetical, the biggest news stories I remember from the recession years are the Tim Tebow playoff game, the BP oil spill, and the Bin Laden raid. A ruder, fuller awakening would only come about once my childhood home had been lost to the trauma of the recession, my parents taking one of their few options to get out of a bad mortgage.)

But hindsight allows the researcher a fuller glimpse of history, and I know now just how brutal the effects of the economic downturn were for Maryland families of all stripes. Homelessness spiked by 20%. Schools lost 1,600 teachers, and in Frederick and Montgomery counties, there wasn’t enough money to vaccinate kids. Public health spending dropped by $30 million from 2008 to 2010, meaning HIV clinics closed and water quality testing halted. The Maryland Center on Economic Policy leveraged this history to warn about the consequences of inaction in the COVID-19 crisis, writing:

Like the current crisis, the Great Recession deeply damaged Maryland communities. Thousands of workers lost their jobs, many faced unaffordable housing costs or even lost their homes, and children across the state saw their formative years marred by physiologically and cognitively taxing trauma. Too often, state and local budget cuts took away vital support right when it was needed most.

– from “Lessons From the Great Recession,” Maryland Center on Economic Policy, Jun 2020

Where there was no money for water testing, there’d be even less for new modes of real estate development, and so I went off assuming that the same suburban built environment in which I had come of age would persist – all Reagan-era malls, fast-food franchises, and unending corridors of subdivisions. And over the course of several years of returning home from school, that assumption held fast. With a construction industry bled of employees and a household sector starved for savings, nothing much changed on the Maryland horizon.

Change was summoned back to Maryland only by the years-long efforts of the state’s biggest institution, which with a lively and focused energy finally coaxed its fellow citizens into beginning the turnaround, a story we’ll cover in Part II.